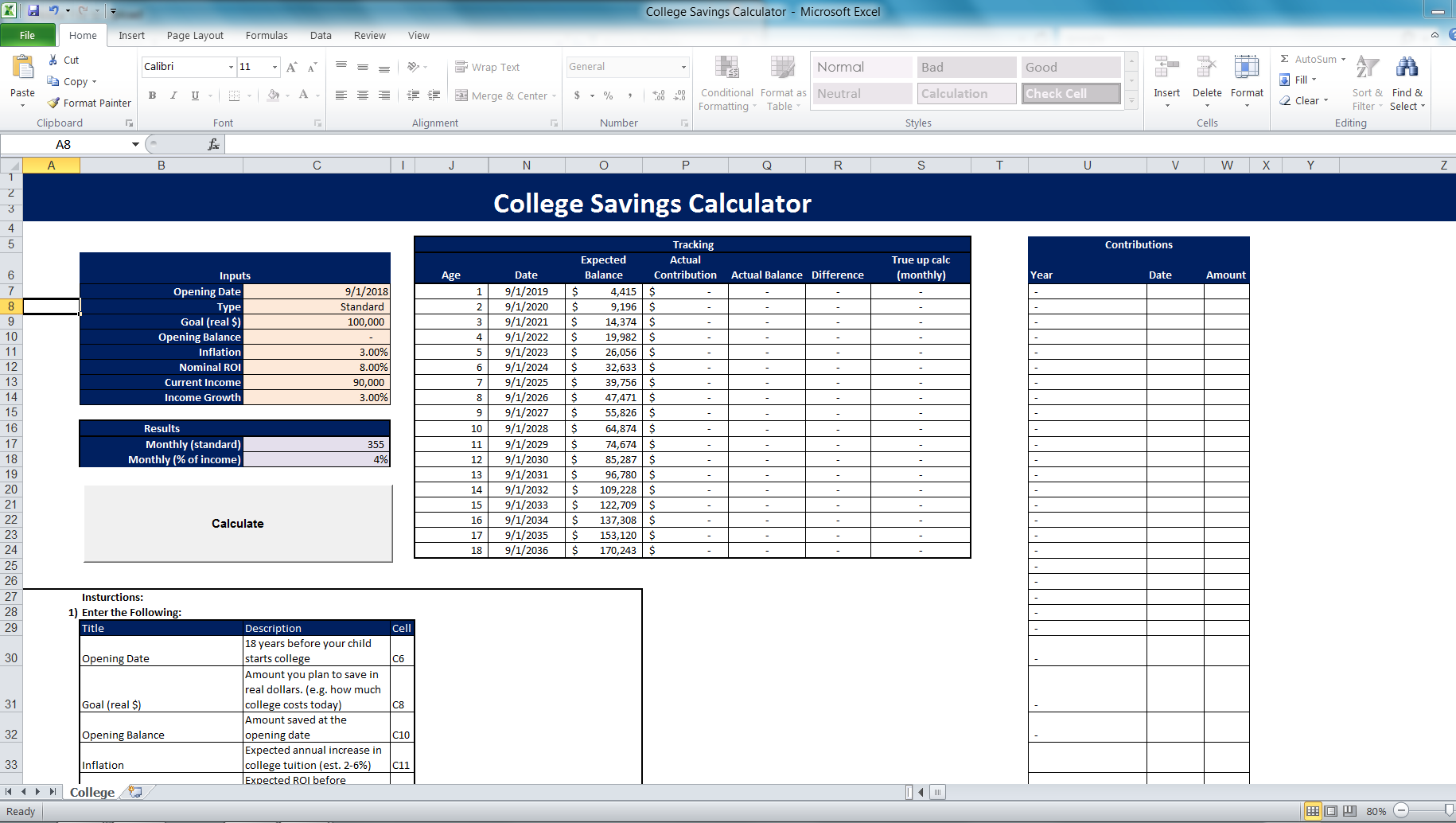

It is important to determine how much you will need in order to comfortably live when you retire. This number could be affected by inflation and an average life expectancy. A nest egg calculator is a tool that can help you calculate how much you will require. You can also factor in inflation and the 4% withdrawal rate. A nest egg calculator is helpful if you're thinking of retiring.

Calculate retirement nest egg

Experts recommend that you have at least 15-25 times your annual income saved for retirement. This figure doesn't reflect inflation and is an estimate. There are also other methods of calculating how much you will need for retirement. A licensed financial professional can help you figure out your ideal retirement nest egg amount.

To calculate how much you'll need to retire comfortably, use an online retirement nest eggs calculator. Some people need 100% of their current income. Others might need more. You can use a nest egg calculator to get an estimate of how much you will need and how long it will take you to reach your goal.

Factor inflation

Inflation is an issue when planning for your future expenditures. Although inflation has been relatively low over the past few years, it can rise rapidly over time so it is important to include this in your calculations. An excellent rule of thumb is to project three percent inflation each year for the next 10-15 years. This number will give you a realistic estimate which will help you calculate how much money it will take to retire comfortably.

Inflation will also need to be considered when calculating how much you will need for your post-retirement income. This includes your pensions, Social Security, rental income and any part-time job you may still be doing. This is because retirement costs will be higher than healthcare costs.

4% withdrawal interest

For a comfortable retirement, you need to have enough savings to last at least 30 year with a 4% withdrawal. Calculating your required annual withdrawals can be done using a calculator, or by downloading a free spreadsheet template. Keep in mind inflation, which averages around 2% annually. To keep up to date with inflation, adjust your withdrawal rate each calendar year.

The 4% rule was initially designed for those who planned to retire at 62 and 65 years. Retirement can come in many forms today. Many people decide to continue working well into their 70s and 80s. Others prefer to retire as soon as possible. Also, medical advances and changes in health can alter your expectations of how long you'll be able to save. The amount that you can withdraw may depend on your investment portfolio.

Average U.S. life expectancy

Americans' life expectancy has increased over the past several decades thanks to improved healthcare and better access to healthcare. The U.S. has a lower life expectancy than other developed countries since 1980 when its average lifespan was 78.9 years. Despite the fact that death rates from COVID-19 were higher, the U.S. is still behind most peers countries. From 2014 to 2019, American life expectancy fell slightly. It increased to 78.1 years between 2014 and 2019. The U.S. might surpass other peer countries by 2020 in terms of life expectancy.

According to the CDC's latest reports, the U.S. suffers from a falling life expectancy compared to other nations. The most significant declines have been in the American Indian and Alaska Native populations. Their life expectancy in 2020-21 will be the same as that of the U.S. populace in 1944. The decrease in life expectancy among White Americans was more rapid than that among Black and Hispanic Americans. This trend has also led to a widening of the gender gap. Women now live up to six years more than men.

FAQ

How much do I have to pay for Retirement Planning

No. You don't need to pay for any of this. We offer free consultations so we can show your what's possible. Then you can decide if our services are for you.

How Does Wealth Management Work?

Wealth Management allows you to work with a professional to help you set goals, allocate resources and track progress towards reaching them.

Wealth managers assist you in achieving your goals. They also help you plan for your future, so you don’t get caught up by unplanned events.

These can help you avoid costly mistakes.

How to Begin Your Search for A Wealth Management Service

If you are looking for a wealth management company, make sure it meets these criteria:

-

Reputation for excellence

-

Is the company based locally

-

Offers complimentary initial consultations

-

Offers support throughout the year

-

A clear fee structure

-

Good reputation

-

It is easy and simple to contact

-

Support available 24/7

-

Offering a variety of products

-

Low charges

-

Do not charge hidden fees

-

Doesn't require large upfront deposits

-

You should have a clear plan to manage your finances

-

Is transparent in how you manage your money

-

Allows you to easily ask questions

-

Have a good understanding of your current situation

-

Understand your goals & objectives

-

Would you be open to working with me regularly?

-

Work within your budget

-

Has a good understanding of the local market

-

Are you willing to give advice about how to improve your portfolio?

-

Are you willing to set realistic expectations?

Why it is important to manage your wealth?

Financial freedom starts with taking control of your money. Understanding your money's worth, its cost, and where it goes is the first step to financial freedom.

It is also important to determine if you are adequately saving for retirement, paying off your debts, or building an emergency fund.

If you don't do this, then you may end up spending all your savings on unplanned expenses such as unexpected medical bills and car repairs.

What are the Benefits of a Financial Advisor?

A financial strategy will help you plan your future. It will be clear and easy to see where you are going.

It provides peace of mind by knowing that there is a plan in case something unexpected happens.

A financial plan can help you better manage your debt. Knowing your debts is key to understanding how much you owe. Also, knowing what you can pay back will make it easier for you to manage your finances.

Protecting your assets will be a key part of your financial plan.

How old should I be to start wealth management

Wealth Management can be best started when you're young enough not to feel overwhelmed by reality but still able to reap the benefits.

The earlier you start investing, the more you will make in your lifetime.

If you are thinking of having children, it may be a good idea to start early.

If you wait until later in life, you may find yourself living off savings for the rest of your life.

Statistics

- According to a 2017 study, the average rate of return for real estate over a roughly 150-year period was around eight percent. (fortunebuilders.com)

- As previously mentioned, according to a 2017 study, stocks were found to be a highly successful investment, with the rate of return averaging around seven percent. (fortunebuilders.com)

- Newer, fully-automated Roboadvisor platforms intended as wealth management tools for ordinary individuals often charge far less than 1% per year of AUM and come with low minimum account balances to get started. (investopedia.com)

- US resident who opens a new IBKR Pro individual or joint account receives a 0.25% rate reduction on margin loans. (nerdwallet.com)

External Links

How To

How to invest after you retire

People retire with enough money to live comfortably and not work when they are done. However, how can they invest it? You can put it in savings accounts but there are other options. You could sell your house, and use the money to purchase shares in companies you believe are likely to increase in value. You could also take out life insurance to leave it to your grandchildren or children.

But if you want to make sure your retirement fund lasts longer, then you should consider investing in property. You might see a return on your investment if you purchase a property now. Property prices tends to increase over time. If you're worried about inflation, then you could also look into buying gold coins. They do not lose value like other assets so are less likely to drop in value during times of economic uncertainty.